Business, 06.11.2020 17:10 ceceshelby2635

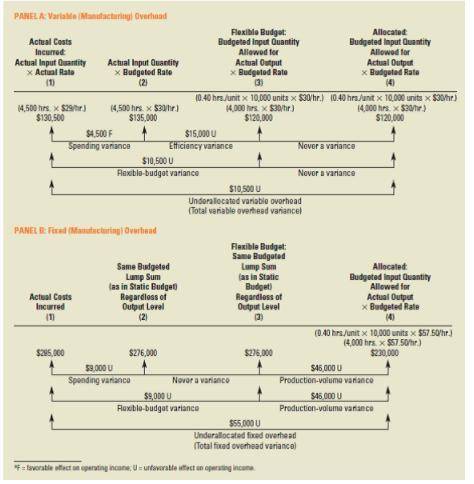

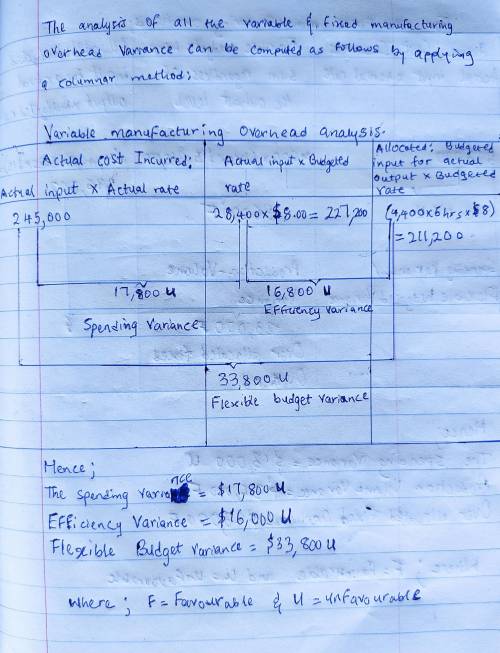

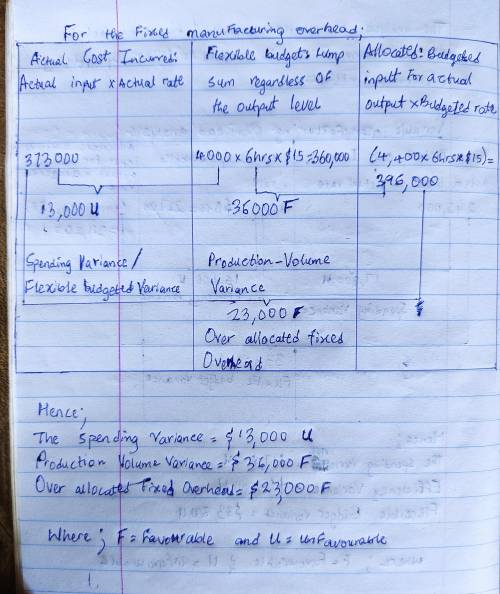

Variable manufacturing overhead incurred was $245,000. Fixed manufacturing overhead incurred was $373,000. Actual machine-hours were 28,400. 1. Prepare an analysis of all variable manufacturing overh

Answers: 2

Another question on Business

Business, 21.06.2019 22:30

Before contacting the news or print media about your business, what must you come up with first ? a. a media expertb. a big budgetc. a track recordd. a story angle

Answers: 1

Business, 21.06.2019 23:30

You are frustrated to find that the only way to contact the customer service department is to make a phone call. the number listed would result in long distance charges to your phone bill. which issue should be addressed by the company to keep its crm in line with your expectations?

Answers: 2

Business, 22.06.2019 11:30

What would you do as ceo to support the goals of japan airlines during the challenging economics that airlines face?

Answers: 1

You know the right answer?

Variable manufacturing overhead incurred was $245,000. Fixed manufacturing overhead incurred was $37...

Questions

Biology, 28.10.2019 03:31

History, 28.10.2019 03:31

Mathematics, 28.10.2019 03:31

History, 28.10.2019 03:31

History, 28.10.2019 03:31

Mathematics, 28.10.2019 03:31