Relax and breathe!

Step-by-step explanation:

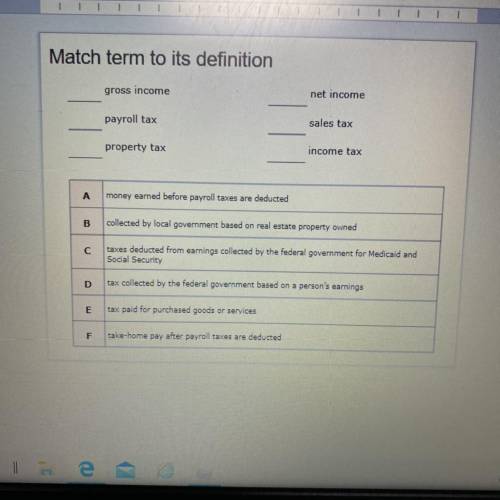

Gross Income - Gross income is the amount of money you earn, typically on a paycheck, before payroll taxes and other deductions are taken out. Gross annual income is the total amount you earn in a year before deductions and taxes.

The gross income on a pay stub would be your hourly wage multiplied by hours worked. You'll also see your year's gross wages on the W-2 form you receive from your employer at tax time. Say your gross wages for a week were $800. However, you take home only $675 in net income or the remainder of your gross income after taxes and other deductions. That's why gross income is also sometimes called pre-tax income.

From the perspective of the Internal Revenue Service (IRS), gross income includes the total amount of income from all sources, which you must report on your income tax return.

Payroll Tax - Payroll taxes are taxes imposed on employers or employees, and are usually calculated as a percentage of the salaries that employers pay their staff. Payroll taxes generally fall into two categories: deductions from an employee's wages, and taxes paid by the employer based on the employee's wages.

Property Tax -Property tax is a tax paid on property owned by an individual or other legal entity, such as a corporation. Most commonly, property tax is a real estate ad-valorem tax, which can be considered a regressive tax. It is calculated by a local government where the property is located and paid by the owner of the property. The tax is usually based on the value of the owned property, including land. However, many jurisdictions also tax tangible personal property, such as cars and boats.

The local governing body will use the assessed taxes to fund water and sewer improvements, and provide law enforcement, fire protection, education, road and highway construction, libraries, and other services that benefit the community.1 Deeds of reconveyance do not interact with property taxes.

Net income - also referred to as net profit, net earnings or the bottom line — is the amount an individual earns after subtracting taxes and other deductions from gross income. For a business, net income is the amount of revenue left after subtracting all expenses, taxes and costs.

Sales Tax - A sales tax is a consumption tax imposed by the government on the sale of goods and services. A conventional sales tax is levied at the point of sale, collected by the retailer, and passed on to the government.

income tax - An income tax is a tax that governments impose on income generated by businesses and individuals within their jurisdiction. By law, taxpayers must file an income tax return annually to determine their tax obligations.12 Income taxes are a source of revenue for governments. They are used to fund public services, pay government obligations, and provide goods for citizens. Certain investments, like housing authority bonds, tend to be exempt from income taxes.3