Answers: 3

Another question on Business

Business, 22.06.2019 01:20

Suppose a stock had an initial price of $65 per share, paid a dividend of $1.45 per share during the year, and had an ending share price of $58. a, compute the percentage total return. (a negative answer should be indicated by a minus sign. do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. what was the dividend yield and the capital gains yield? (a negative answer should be indicated by a minus sign. do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.)

Answers: 2

Business, 22.06.2019 10:50

Choose the statement that is incorrect. a. search activity occurs only in markets where there is a shortage. b. when a price is regulated and there is a shortage, search activity increases. c. the time spent looking for someone with whom to do business is called search activity. d. the opportunity cost of a good is equal to its price plus the value of the search time spent finding the good.

Answers: 3

Business, 23.06.2019 07:50

To record a 6% stock dividend, accountants use to record a 55% stock dividend, accountants use a. par value per share; market price per share b. par value per share; par value per share c. market price per share; market price per share d. market price per share; par value per share

Answers: 1

Business, 23.06.2019 15:00

Value economics capital scarcity opportunity cost wealth labor trade-offs standard of living good a. condition of not having enough resources to produce all the things people want b. alternative choices made by consumers in the marketplace c. sum of those economic products that are tangible, scarce, useful, and transferable d. tools, equipment, machinery, and factories used in the production of goods and services e. tangible item that is economically useful or that satisfies an economic want f. quality of life based on the ownership of the necessities and luxuries that make life easier g. people with all their efforts, abilities, and skills h. cost of the next-best alternative use of money, time, or resources when one choice is made rather than another i. study of how people try to satisfy their needs through the careful use of scarce resources j. worth that can be expressed in dollars and cents

Answers: 1

You know the right answer?

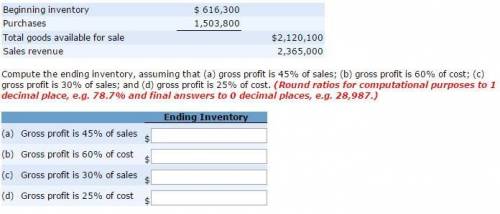

Compute the ending inventory, assuming that (a) gross profit is 45% of sales, (b) gross profit is 60...

Questions

Mathematics, 01.08.2019 09:00

History, 01.08.2019 09:00

History, 01.08.2019 09:00

English, 01.08.2019 09:00

Mathematics, 01.08.2019 09:00

Mathematics, 01.08.2019 09:00

History, 01.08.2019 09:00

Mathematics, 01.08.2019 09:00

Advanced Placement (AP), 01.08.2019 09:00

Mathematics, 01.08.2019 09:00